Source: Galaxy Research

Translated by: BitpushNews

Crypto Treasury Trends

The trend of public companies establishing cryptocurrency treasuries is expanding from Bitcoin to more crypto tokens, with allocation scales continuously growing.

In just the past week, two public companies announced they will purchase XRP for their treasury, and another company stated it is buying ETH as a reserve.

Bitcoin treasury companies have been headline news for most of this year, with Strategy (formerly Microstrategy) leading the way. VivoPower and Nasdaq-listed Webus announced plans to launch XRP treasuries of $100 million and $300 million respectively, while SharpLink announced establishing a $425 million ETH treasury.

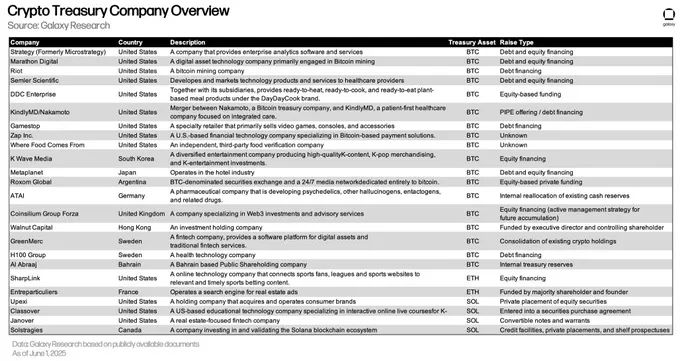

Including these companies, Galaxy Research has compiled 28 cryptocurrency treasury companies:

20 focused on BTC, 4 focused on SOL, 2 focused on ETH, 2 focused on XRP.

Cryptocurrency Treasury Company Overview

Our View

Given the momentum of existing companies and the market's apparent strong interest in funding these companies with substantial scale and diverse assets, the trend of cryptocurrency treasuries is expected to continue developing.

However, as more cryptocurrency treasury companies come online, skepticism continues to rise.

The primary concern is the source of funding for partial purchases: debt.

Some companies rely on borrowed funds, mainly zero-interest and low-interest convertible notes, to purchase treasury assets.

At maturity, these notes can be converted into company equity by investors, provided the notes are "in the money" (i.e., when the company's stock price exceeds the conversion price, making equity conversion economically advantageous). However, if the maturity date arrives and the notes are "out of the money", additional funds will be needed to cover the liability—the source of concern for treasury company strategies.

Additionally, though less mentioned, there is a risk that these companies may lack sufficient cash to pay their debt interest.

Regardless of the scenario, treasury companies have four main options. They can:

Sell their cryptocurrency reserves to supplement cash, which could harm asset prices and potentially impact other treasury companies holding the same assets.

Issue new debt to cover old liabilities, effectively refinancing debt.

Issue new stocks to cover liabilities, which is similar to their current method of funding treasury asset purchases through equity financing.

If their cryptocurrency reserves' value fails to fully cover liabilities, they will enter default.

In the worst-case scenario, each company's path will depend on the specific circumstances and market conditions at the time; for example, treasury companies can only refinance when market conditions permit.

Contrary to treasury fund sources is equity sales, where treasury companies issue stocks to fund asset purchases. Equity sales used to supplement asset purchases are less concerning from a broader perspective, as in this method, the company has no default obligation and does not incur liabilities for asset purchases.

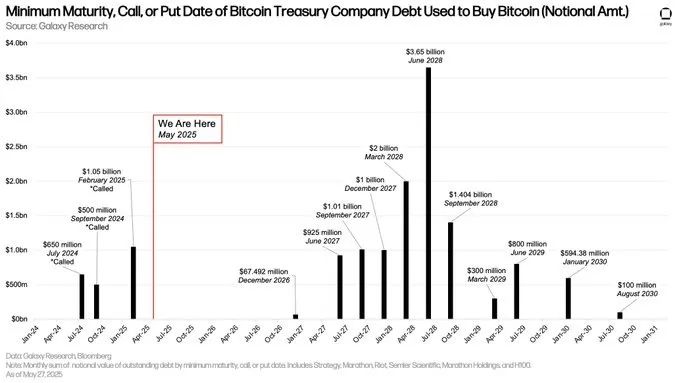

In our recent report on the crypto leverage landscape, we examined the scale and maturity timeline of debt issued by some Bitcoin treasury companies.

Based on our findings, we believe that there is not an imminent threat as widely perceived by the market, as most debt matures between June 2027 and September 2028 (as shown in the chart below).

The chart above tallies the debt issued by Bitcoin treasury companies to purchase Bitcoin and lists the earliest dates these debts might be required to be repaid (maturity/redemption/exercise dates), along with their corresponding nominal debt amounts.

Considering the industry's past history with leverage, concerns about treasury companies' debt-driven strategies are not unreasonable, but currently, we believe this approach poses no significant risks.

However, as debt matures and more companies adopt this strategy, potentially taking higher-risk approaches and issuing shorter-term debt, this situation may not remain unchanged.

Even in the worst-case scenario, these companies will have a range of traditional financial options to escape difficulties, which may not end with selling treasury assets.

– Galaxy On-chain Analyst @ZackPokorny_