Written by: kushagra

Translated by: Luffy, Foresight News

Every day, we see new cryptocurrency treasury strategy tools emerging. This article will analyze the performance of Bitcoin as a corporate treasury strategy and key trends in crypto strategies based on Private Investment in Public Equity (PIPE).

Every region will launch its own "Bitcoin" strategy, but what concerns me are the potential tail assets that might adopt similar strategies. Bitcoin works well as a reserve asset, but what about your beloved L1 or L2? That makes no sense. After all, who would be the marginal buyer of the 50th zkEVM L2? Not to mention, tail assets suffer from low liquidity issues, and the book gains market participants see may not be truly realizable. So, friends, be cautious.

Operational Mechanism

There are primarily three paths to building such treasury tools:

Business Transformation: Companies on the brink of bankruptcy pivot to crypto financial service providers, implementing crypto strategies (such as Solana staking);

Mergers and Acquisitions: Integrating private companies into small and medium-sized companies listed on NASDAQ/NYSE;

SPAC Merger: Merging through Special Purpose Acquisition Companies (SPAC) to redefine business and treasury strategies.

Regardless of the path, all strategies require Private Investment in Public Equity (PIPE) and convertible debt financing. Here's a typical PIPE operation:

Target shell companies: Usually SPAC tools or failed small and medium-sized companies publicly traded on NASDAQ or NYSE

Collaborate with the company to create reserves for Bitcoin or any other crypto asset

Request investment banks to issue/construct two tools: i) traditional PIPE and ii) convertible bonds

Traditional PIPE: Directly sell common or preferred shares to qualified investors at a fixed price (usually at a discount)

Convertible Bonds: Issue convertible bonds or convertible preferred shares that investors can convert to the issuing company's common shares within a certain period or under specific conditions. These typically provide downside protection and partially reduce upside returns.

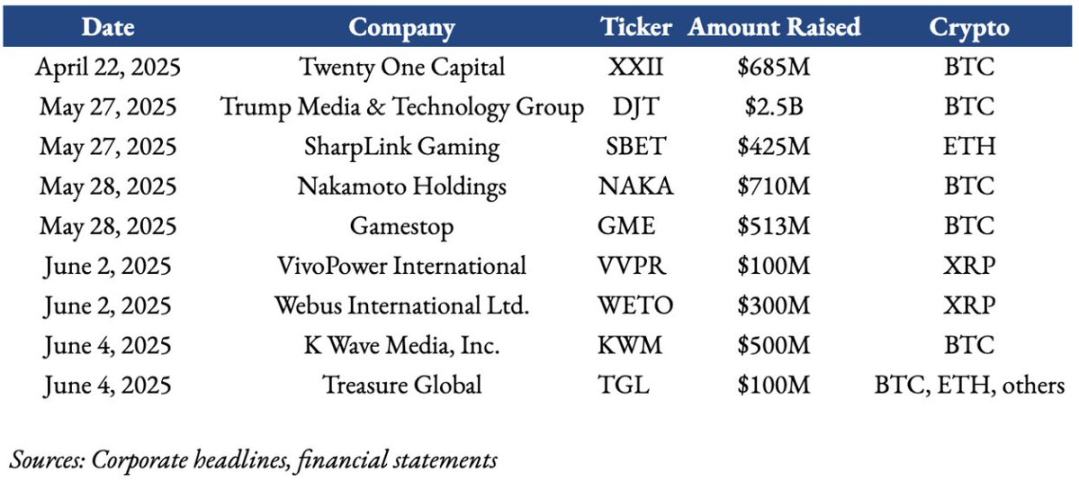

For example, Trump Media & Technology Group (DJT) adopted the following structure:

Raised $1.44 billion by selling nearly 56 million shares (at $25.72 per share);

Issued $1 billion 0% convertible senior secured bonds maturing in 2028 (with a conversion price of $34.72 per share).

This is a hybrid structure of stock dilution and senior convertible debt, combining the characteristics of PIPE and convertible bonds.

Note: Compared to other issuance methods, PIPE is less regulated by the SEC but may lead to dilution of existing shareholders' equity. These shares come with registration rights, meaning the company must submit a registration statement to the SEC, allowing PIPE investors to resell shares to the public after the lock-up period.

Investor Framework

You might wonder why investors are willing to participate in such issuances? The reasons can be summarized in three points:

Team Intellectual Property: The industry influence of the chairman or core team is crucial. For example, an ETH strategy launched by Joe Lubin (Ethereum co-founder) can easily be compared to an "Ethereum version of Microstrategy". After witnessing MSTR's success, investors eagerly participate in the ETH strategy due to Joe's industry standing, given ConsenSys's critical role in the Ethereum ecosystem.

Asset Quality: The choice of reserve assets is crucial. A wave of tail assets (such as tokens in the top 50 by market cap) being incorporated into small enterprise treasuries is expected. However, these tail asset strategies carry higher risks due to their typically higher volatility compared to Bitcoin.

Crypto Premium: The ability of such PIPE tools to raise funds on a large scale is not because Bitcoin or Ethereum's value in corporate strategies "suddenly increased 3-4 times", but because traditional hedge funds and native crypto institutions rush in, fearing to miss out (FOMO) on current first and second-market arbitrage opportunities. Admittedly, these strategies may generate returns or leverage effects through staking and lending, but can this support a premium 3 times the asset net value? Probably not.

Overview of Corporate Crypto Treasury Transactions in the Past Two Months

To date, the most controversial treasury transaction is the case of Trump Media. This has raised questions about "strategic Bitcoin (or digital asset) reserves" - how to handle potential conflicts of interest? At least in the short term, inspired by Microstrategy (MSTR) and Metaplanet (3350.T), both private and public investors expect such financing to bring medium to short-term high returns.

MSTR initially used Bitcoin as a value storage and anti-inflation tool; today's crypto PIPE aims to achieve more proactive management and yield generation through staking and lending. Private investors' demand for crypto PIPE is almost fanatical, as such transactions often see stock prices rising 2-10 times upon announcement.

Performance of Corporate Crypto Treasury Strategies

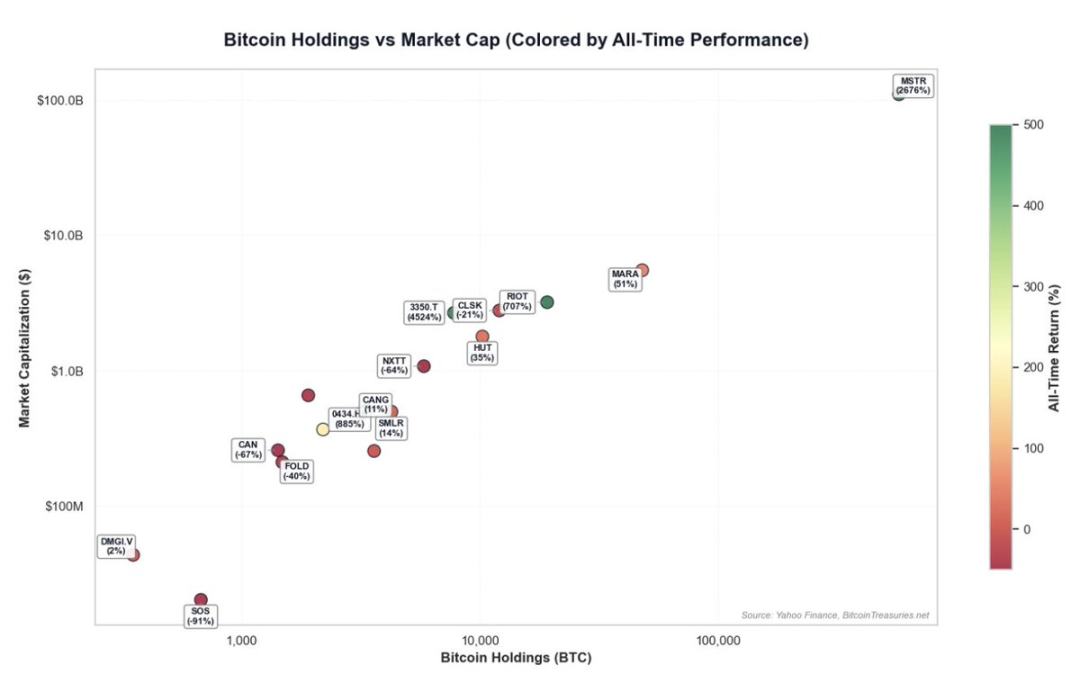

Although history cannot predict the future, there is extensive data available to analyze Bitcoin strategies. Here's a performance study of pure Bitcoin treasury strategies for 17 listed companies:

List of 17 companies with Bitcoin holdings exceeding 30% of company market value and holding over 300 BTC

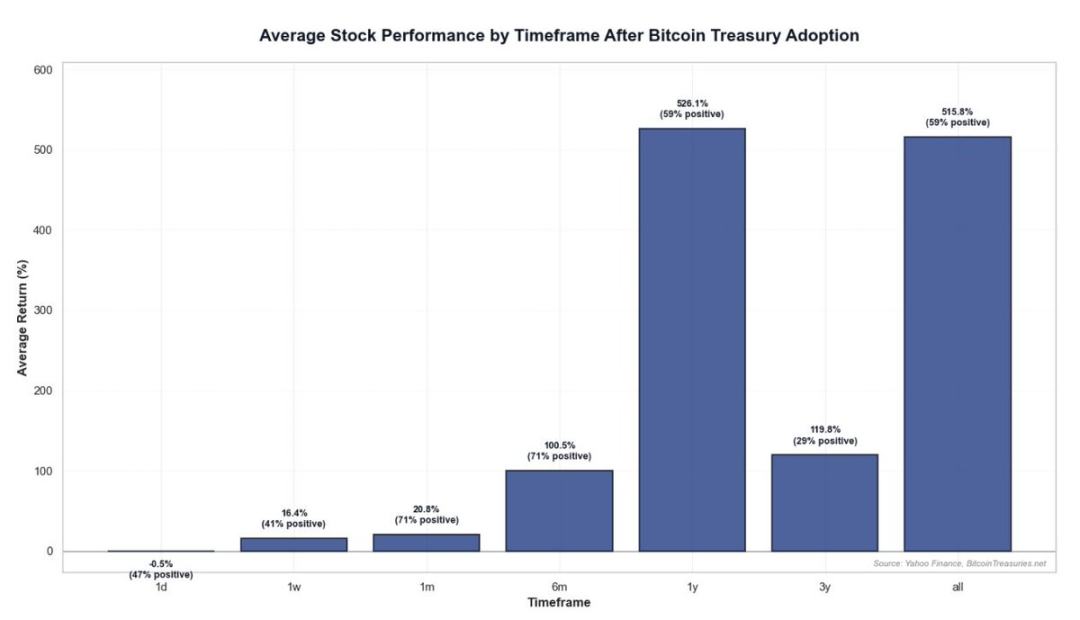

To date, the most successful company adopting this strategy is Microstrategy, which was the earliest to venture into corporate Bitcoin strategies. However, with the introduction of Bitcoin ETFs and new treasury strategies, its "Bitcoin/market value" premium may gradually fade. In the short term, announcements of Bitcoin fund strategies often increase the likelihood of short-term or even long-term returns. Return rate differences are significant, even within different time frames. However, performance declines over time:

1-year average return: 526% (59% of companies profitable);

3-year average return: 119% (only 13.64% of companies profitable);

Historical average return: 515% (59% of companies profitable).

Note: Median returns are significantly lower than the mean, indicating that extreme values have pulled up the overall average. From 2020-2025, Bitcoin outperformed most asset classes, which was the core driver of these companies' high returns.

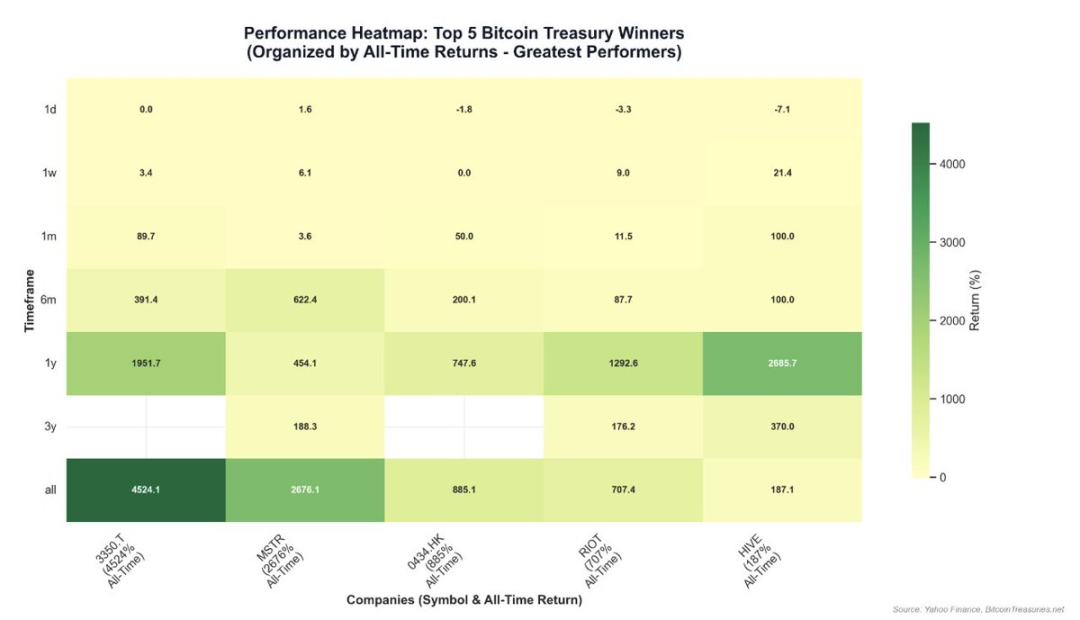

Performance Heatmap of Bitcoin Strategies

Success Cases: Companies with strong community consensus, ability to enhance "Bitcoin per share" and create financial engineering opportunities perform excellently.

Failure Cases: Companies like SOS Limited (formerly a crypto mining company transformed into commodity trading) performed poorly due to core business challenges and ineffective Bitcoin strategies. It's evident that "pure Bitcoin strategy" companies are more market-recognized than "small allocation" companies.

Risk Warning: Bitcoin-related companies may face extreme volatility and drawdowns, but opportunities for turnaround may arise when company net asset value (NAV) exceeds market value. Note: For companies on the brink of bankruptcy, holding a small amount of Bitcoin on the balance sheet alone cannot reverse the decline.

Conclusion

With Circle's successful IPO as a pure stablecoin company, the stock market and crypto market are accelerating their integration. It is expected that more high-quality crypto companies will go public in the future, and more crypto strategy tools will emerge. Given the recent market enthusiasm for crypto strategies, investors can capture opportunities through the following framework: team influence, asset quality, and the sustainability of crypto premiums, while conducting in-depth analysis of specific projects.

However, when strategies involve tokens outside the top 20 by market cap, extreme caution is necessary. These tokens not only lack the hard asset properties of Bitcoin but often lack sustained net buying demand. Structurally, investors must clarify: 1) the underlying business strategy the company is implementing; 2) the capital structure of the transaction (debt, convertible bonds, PIPE); and 3) net asset value per share.