Plasma is a blockchain that only supports stablecoins. How to redefine payment infrastructure with zero transaction fees, Bitcoin-level security, and a vision for mainstream finance. Kairos Research is an investor in Plasma. The information provided by Kairos Research, including but not limited to research, analysis, data or other content, is for reference only and does not constitute investment advice, financial advice, trading advice or any other form of advice. Kairos Research does not recommend buying, selling or holding any cryptocurrency or other investment asset.

The rise of stablecoins and the need for dedicated infrastructure

Stablecoins have rapidly evolved from a niche application to one of the most important innovations in the crypto market and have become an emerging medium for global payments. In 2024 alone, USD-anchored stablecoins, represented by Tether's USD₮, processed transactions worth up to $15.6 trillion, equivalent to 119% of Visa's payment volume in the same period. In addition, according to the latest data, USD₮ has about 400 million users in emerging markets. This surge heralds the arrival of the "stablecoin singularity": digital dollars circulate freely like information and are reshaping the way money flows.

We believe that the full integration of stablecoins into all levels of the global payment system (including P2P, B2B and P2B) has the potential to greatly improve people's daily lives. Ideally, blockchain can significantly shorten payment settlement time, bypassing intermediaries that charge high intermediary fees and can even freeze funds at any time. However, the current mainstream blockchains are not optimized for stablecoins, resulting in high transaction fees on networks such as Ethereum, forcing users to turn to more centralized, slightly lower-cost alternatives such as Tron.

This is where Plasma comes in - a blockchain tailor-made for stablecoins. Plasma is focused on one thing: making stablecoins (like USD₮) transfers fast and free. Unlike general L1 chains that try to support a variety of applications at the same time, Plasma focuses on stablecoin payments, thereby unlocking advantages at the technical and economic levels and is expected to become the standard payment layer for the global digital dollar. Because its functionality is limited to stablecoin payments, Plasma can maximize throughput, minimize latency, and completely eliminate transaction fees for USD₮ users. The ultimate goal is to achieve a transfer experience as simple and smooth as texting, but it may also have far-reaching secondary and tertiary effects.

Zero-fee USD₮ transfers: a powerful magnet for liquidity

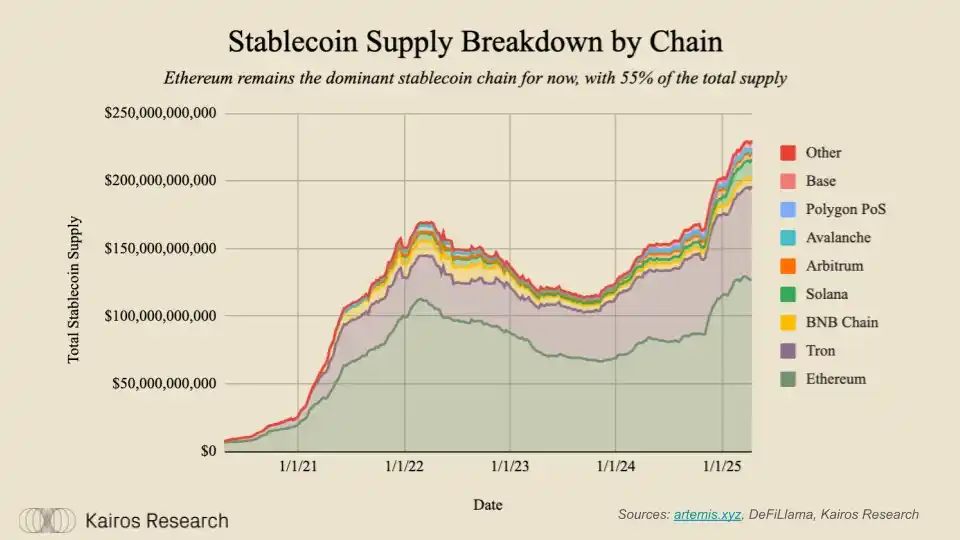

Although Ethereum is currently the blockchain with the largest issuance of stablecoins, its architecture makes stablecoin transactions expensive, and each transfer often requires several dollars, which has pushed many users to the Tron network with lower transfer fees. Tron has seized this demand and promoted its low-cost transaction model in emerging markets. According to Artemis data, Tron processed approximately $5.46 trillion in USD₮ transfers through 750 million transactions in 2024. If Tron's rise relies on its low-fee advantage, then Plasma's "zero fee" model goes a step further, allowing applications to skip the trouble of paying Gas, which may trigger a larger wave of adoption.

For users, "zero fees" is not just about saving money, it can also inspire new use cases: when sending $5 no longer requires a $1 fee, micropayments become feasible. Cross-border remittances can also be fully received without being charged high fees by intermediaries. Merchants can receive stablecoin payments without having to hand over 2-3% of the transaction amount to the billing and credit card networks. In short, Plasma's free transfers break the barriers that previously limited stablecoins to transaction scenarios and open up channels for daily consumption scenarios. Thanks to the support of the Tether ecosystem, Plasma's incentive mechanism is perfectly aligned with the promotion of USD₮. Liquidity attracts more liquidity. Once users realize that they can transfer value freely on Plasma, it may attract stablecoin flows from the entire crypto market, further consolidating its position as the preferred channel for digital dollars.

In addition, the growing USD₮ deposits and native issuance capabilities on Plasma make it an ideal expansion ecosystem for existing DeFi protocols. Currently, protocols that focus on stablecoins such as Curve and Ethena have announced plans to deploy to the EVM-compatible Plasma network. At the same time, the network effect of USD₮ as a mainstream stablecoin makes it the default pricing unit for Bitcoin spot pairs on mainstream exchanges. For example, since August 2017, the cumulative trading volume of the BTC/USD₮ trading pair on Binance has reached 4.9 trillion US dollars. As BTC cross-chain bridge technology matures and trust assumptions are reduced, we believe that more liquid Bitcoin will enter the Plasma network in the future, forming a synergistic effect with the familiar pairing of USD₮, which is expected to stimulate more trading activities, especially when users align centralized exchanges and on-chain BTC prices through arbitrage.

Comprehensively surpassing Ethereum, Tron and traditional payment rails

So how does Plasma perform compared to existing crypto networks and traditional fintech infrastructure? It can be said that Plasma aims to surpass both in multiple dimensions.

Ethereum: Ethereum has a diverse DeFi ecosystem, but at the cost of tight block space and high gas fees. Even a simple USD₮/USDC transfer costs several dollars. Although stablecoins started on Ethereum and account for a large amount of on-chain usage (about 35-50%), they are mainly large transactions, often excluding small users. Although Layer-2 Rollup helps to reduce fees, Plasma's approach is more radical - a chain built solely for stablecoins, with speed and cost optimization from the underlying architecture. Since it does not need to "support everything", Plasma can devote all its resources to the transfer processing of stablecoins, thus avoiding congestion problems on general-purpose chains.

Tron: Tron has become the main network for stablecoins, accounting for a huge amount of Tether's transaction volume, thanks to its low fees and faster confirmation speed. Tron's TRC-20 USD₮ has accumulated 22 billion transfers, far exceeding Ethereum's ERC-20's 2.6 billion, indicating that high-quality user experience (especially low-cost and fast transfers) can significantly increase market share. Plasma has taken user experience to a new level: while Tron still requires paying $2-3 or even staking TRX to get free or discounted transactions, Plasma is completely free of fees for USD₮ transfers.

In addition, Tron's DPoS architecture has long been criticized for being too centralized, with only 27 "semi-permissioned" verification nodes, and its network relies on native tokens for payment of fees and governance. Plasma, on the other hand, uses Bitcoin-level security mechanisms and supports payment of fees in stablecoins themselves (if necessary), which is undoubtedly a more user-friendly design. If Tron is the current "stablecoin chain", then Plasma is preparing to surpass it with a better user experience and economic model.

PayPal and traditional financial payment channels: Traditional payment processors and fintech platforms are also actively paying attention to the development of stablecoins. PayPal launched its own US dollar stablecoin PYUSD in 2024, and plans to integrate it into more than 20 million merchants by 2025, showing the market's strong demand for better digital US dollar payment channels. However, PayPal's network and similar systems such as Visa and ACH still have problems such as fees, transfer limits, processing delays and geographical restrictions. Under the current system, PayPal merchants can charge up to 5.4% + $0.30 per transaction, and cross-border payments also face exchange rate differences and waiting times. Although PayPal's stablecoin will reduce the friction costs of currency exchange, it remains to be seen whether it will significantly reduce merchant fees.

In contrast, Plasma solves this problem from a crypto-native perspective: it uses an open infrastructure, no intermediaries, and no "tolls" for fund transfers. Anyone with a crypto wallet can use Plasma to make stablecoin payments as easily as using email, without the need for a bank account or payment application as an intermediary. This openness and neutrality may attract fintech platforms and even traditional financial institutions to build clearing systems on Plasma, just as the Internet's TCP/IP protocol eventually became the standard for data transmission.

Huge market opportunity for stablecoin payments

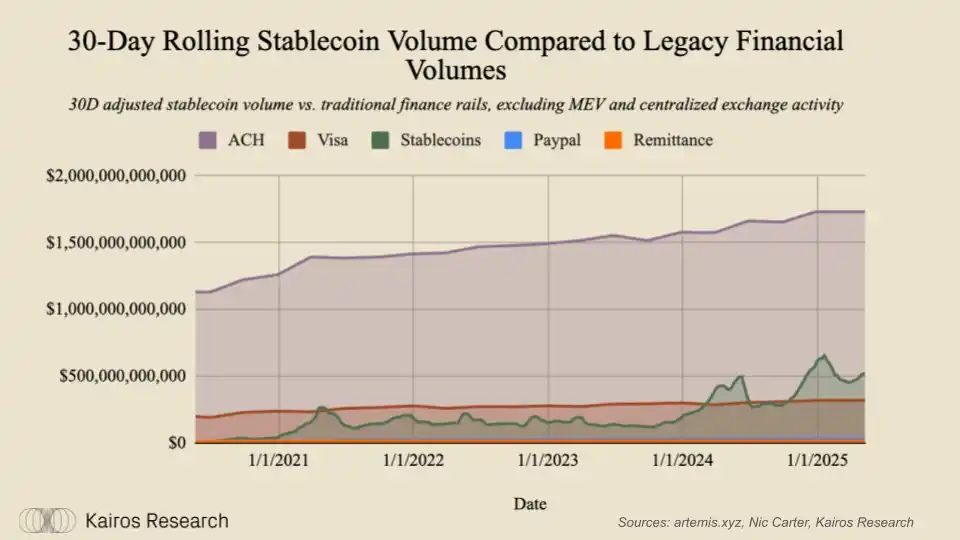

The timing of Plasma’s launch is perfect, as the market for stablecoin-based payments is not only large, but also rapidly expanding. The total stablecoin supply now exceeds $230 billion, accounting for about 1.27% of the US M1 money supply and about 1.08% of M2. This may not seem like much, but in January alone, stablecoin supply grew by 14%, and has maintained a CAGR of 38% since 2018. If this trend continues, the volume of stablecoins could approach the total monetary volume of some G20 countries in a few years.

More tellingly, the total volume of stablecoin transfers in 2024 has surpassed that of several major bank card networks, second only to the Federal Reserve’s ACH transfer system. This suggests that we are rapidly moving toward a reality where large-scale global capital flows are highly dependent on crypto infrastructure rather than traditional payment channels (although this remains highly speculative).

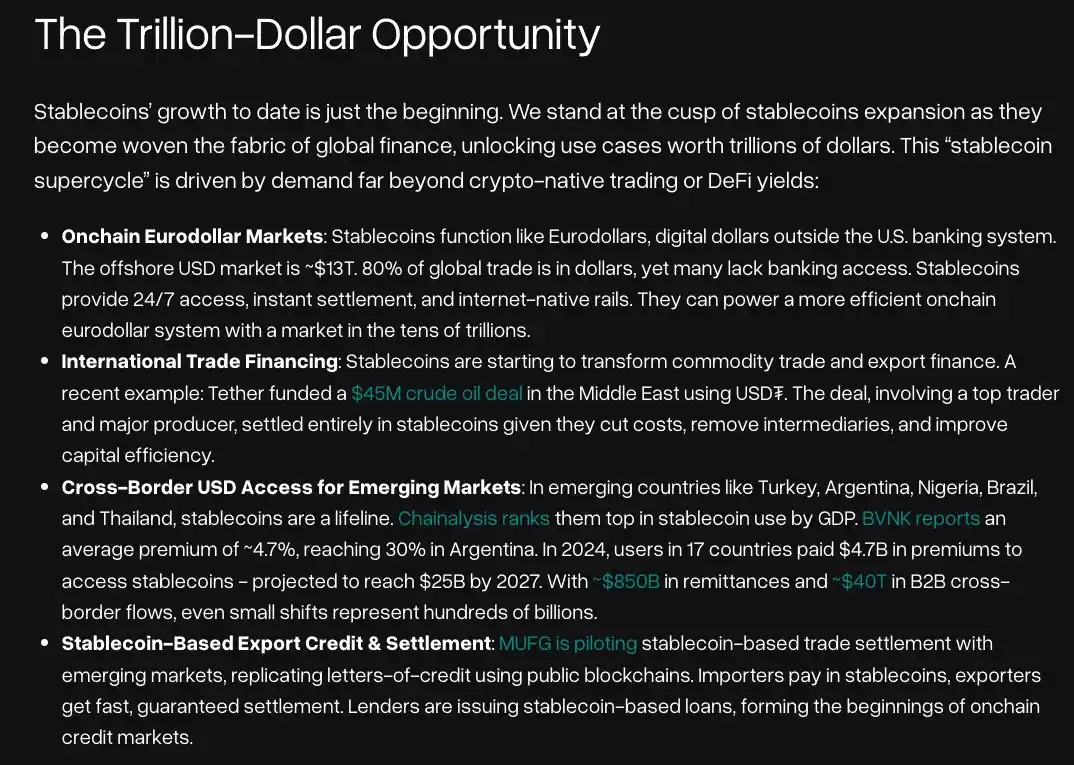

While the dominant use of stablecoins is still focused on transactions and DeFi, the next important growth area is traditional commerce and general payments. This area covers a wide range of sectors, from remittances (annual market size of approximately $700 billion), to e-commerce payments (trillions of dollars per year globally), to B2B cross-border trade (over $30 trillion). We have seen that stablecoins are gradually entering retail and commercial payment scenarios. For example, PayPal emphasized the practical application value of stablecoins at its 2025 Investor Day. The company is working to encourage companies to pay overseas suppliers through PYUSD, thereby avoiding actual fund transfers and completing settlements only through updates between ledgers. This not only saves merchants processing time and fees, but also keeps merchants in the PayPal ecosystem-this is crucial because currently up to 80% of merchant payments flow out of the PayPal network and into bank accounts immediately after they arrive.

Consider the merchant payment scenario.

As mentioned earlier, merchants typically lose 2-3% in fees on each transaction. This cost can be nearly eliminated if stablecoins are used on a zero-fee network. Assuming the merchant is willing to accept USD, or can convert it to local currency through a crypto exchage, a merchant in Nigeria, for example, selling goods to a German customer can be settled instantly in USD stablecoins directly through the Plasma network without having to deal with credit card fees or wait for international wire transfers to arrive. In fact, Tether recently facilitated a $45 million Middle Eastern crude oil transaction, demonstrating to both parties the efficiency of stablecoin settlement.

The global trade market is worth more than $30 trillion, and the U.S. dollar has been deeply integrated as a global settlement currency, accounting for 80%-90% of global transactions. This is a huge pie, and even if Plasma only occupies a small part of it, it is likely to carry billions of dollars in value transfer every day, thus forming a strong network effect and gradually becoming irreplaceable.

Value capture without fees: Rethinking the cryptoeconomic model

Given that the core functionality provided by Plasma is the zero-fee USD₮ transfer, an obvious question is: how is the value of the network captured? This involves a completely new economic model that prioritizes growth and utility, deferring monetization to indirect channels - just like how Robinhood quickly attracted a large number of users and trading activities through "zero commission trading".

In traditional smart contract chains, value is accumulated through gas fees (e.g., Ethereum’s billions of dollars in fees per year drive ETH destruction and staking income; Tron has also accumulated $1.36 billion in fees in six months). Plasma subverts this model and abandons charging fees for USD₮ transfers to drive early growth. Its assumption is that a network that carries a large amount of dollar-denominated economic activity will achieve value capture through secondary and tertiary means, rather than charging users on each transaction.

This is also similar to the free platform expansion path of Web2 - first provide free services to gain billions of users, and then monetize through marginal means. For example, Venmo does not charge for transfers, but earns revenue through credit card payments, instant withdrawals, and cryptocurrency purchases. It is worth reminding that even the most mainstream Web2 tools often have zero marginal usage costs.

For Plasma, we believe there are two main core value capture mechanisms:

Issuance and Issuer Incentives

Stablecoin issuers have an incentive to mint and redeem on the most active chains, which is a big advantage for Plasma. The more deeply stablecoins are integrated into business and trade activities, the more frequently they are minted and redeemed. Millions of transactions per day, even if only 1 cent of on-chain fees are charged per transaction, will quickly accumulate to form sustainable network revenue. In addition, with the launch of USD₮0 (through LayerZero to achieve unified liquidity of USD₮ across multiple chains), Plasma is expected to become the main issuance layer of USD₮.

DeFi + MEV (Maximum Extractable Value)

If the massive inflow of BTC and stablecoins attracts DeFi applications, the entire Plasma ecosystem will prosper. Standard DEXs, lending platforms, and futures markets all require high-quality assets and collateral. As Solana has shown in recent months in terms of real economic value (REV), activities such as token minting, trading, arbitrage, and liquidation can generate enough on-chain activity to support the free transfer model.

Plasma’s user base also has more “real world utility” and may be more willing to use multiple fiat stablecoins. We expect more assets (such as commodities and securities, both public and private markets) to be tokenized in the coming year, making Plasma more attractive to institutional users.

In addition, many investors believe that MEV will become the main value driver of the network in the long term because it is a core component of permissionless finance. In simple terms, MEV can be understood as the premium that people are willing to pay in order to prioritize the execution of state changes.

The main trading pairs of the top five non-stablecoin crypto assets (BTC, ETH, SOL, XRP, BNB) are all denominated in USD₮, so it can be inferred that the chain that can gather the most USD₮ activities will also attract more non-native assets to migrate to this chain for trading. Although this trend has not yet been fully realized, considering the currency network effect (especially USD₮), this idea is not far-fetched, especially for BTC.

Going back to the example of BTC, if more BTC activity occurs on Plasma, it will lead to more sustained network usage, allowing validators and stakers to earn more benefits, rather than relying on periodic Meme coin transactions. For example, in Solana's highest trading volume month (January 2025), the total DEX trading volume reached 379 billion US dollars; during the same period, the BTC/USD₮ spot trading pair on Binance had a trading volume of 144 billion US dollars. Since the fees of DEX depend on the degree of network congestion and pool settings, the threshold is low and the fees are often lower than those of centralized exchanges (the latter has an average fee of about 0.1%). Although the mechanisms are different, the trend of decentralized transactions engulfing the share of centralized transactions is irreversible. Ultimately, most transactions will occur in places that do not require permission, and MEV will play a key role in this.

Most importantly, Plasma amplifies network effects by eliminating transaction fees.

The history of successful networks tells us that user use is a prerequisite for monetization. In the crypto world, the value of a blockchain’s native assets is often a proxy for the size and activity of its community. If Plasma becomes the center of stablecoin transactions, even if USD₮ transfers continue to be free, the value of its ecosystem will still be reflected. This model is a long-term strategy: occupy the market first, then explore profitability. What’s more, Plasma substantially improves the practicality of the “digital dollar”, which naturally fits the interests of large capital institutions that intend to promote the globalization of the dollar.

Alignment with US Policy: The Potential of the GENIUS Act

As crypto adoption matures in the U.S., compliance becomes increasingly critical, and now is a good time to follow the policy window and embrace regulatory dividends. It is particularly noteworthy that the emergence of Plasma coincides with the U.S. lawmakers’ efforts to bring stablecoins into the federal regulatory framework.

This week, the U.S. Senate advanced the GENIUS Act, a bipartisan bill that aims to establish a comprehensive federal regulatory system for stablecoins. If the legislation is successful, the bill will clearly stipulate how to issue and manage dollar stablecoins under U.S. law, thereby incorporating them into the mainstream financial system rather than continuing to exist as a regulatory gray area.

Although the friendly attitude of regulators under the Trump administration has had a positive impact on the industry, clear crypto legislation will provide innovators with a predictable policy environment in the long term. This is the turning point that financial institutions have long been waiting for, and it may clear the way for them to fully embrace stablecoins.

Plasma is a natural fit with this regulatory trend. Its focus on fiat-backed stablecoins, rather than the more controversial and complex algorithmic stablecoins, makes it likely that Plasma will be one of the first networks to benefit once parallel bills such as the GENIUS Act or the House’s STABLE Act are passed.

It is worth mentioning that US policymakers who are concerned about the global dominance of the US dollar may view networks such as Plasma as positive assets. By making the US dollar stablecoin more useful and accessible, Plasma essentially expands the global influence of the US dollar in a transparent way. Compared with domestic and foreign central bank digital currencies (CBDCs), the path of USD₮ liquidity + BTC security taken by Plasma is more likely to be seen as enhancing the power of the "digital dollar".

Currently, more than 98% of the stablecoin market value is backed by the US dollar, and this trend is likely to continue. The GENIUS Act is expected to require stablecoin issuers to fulfill strict measures such as reserve requirements, audit obligations, and redemption policies to protect consumer interests.

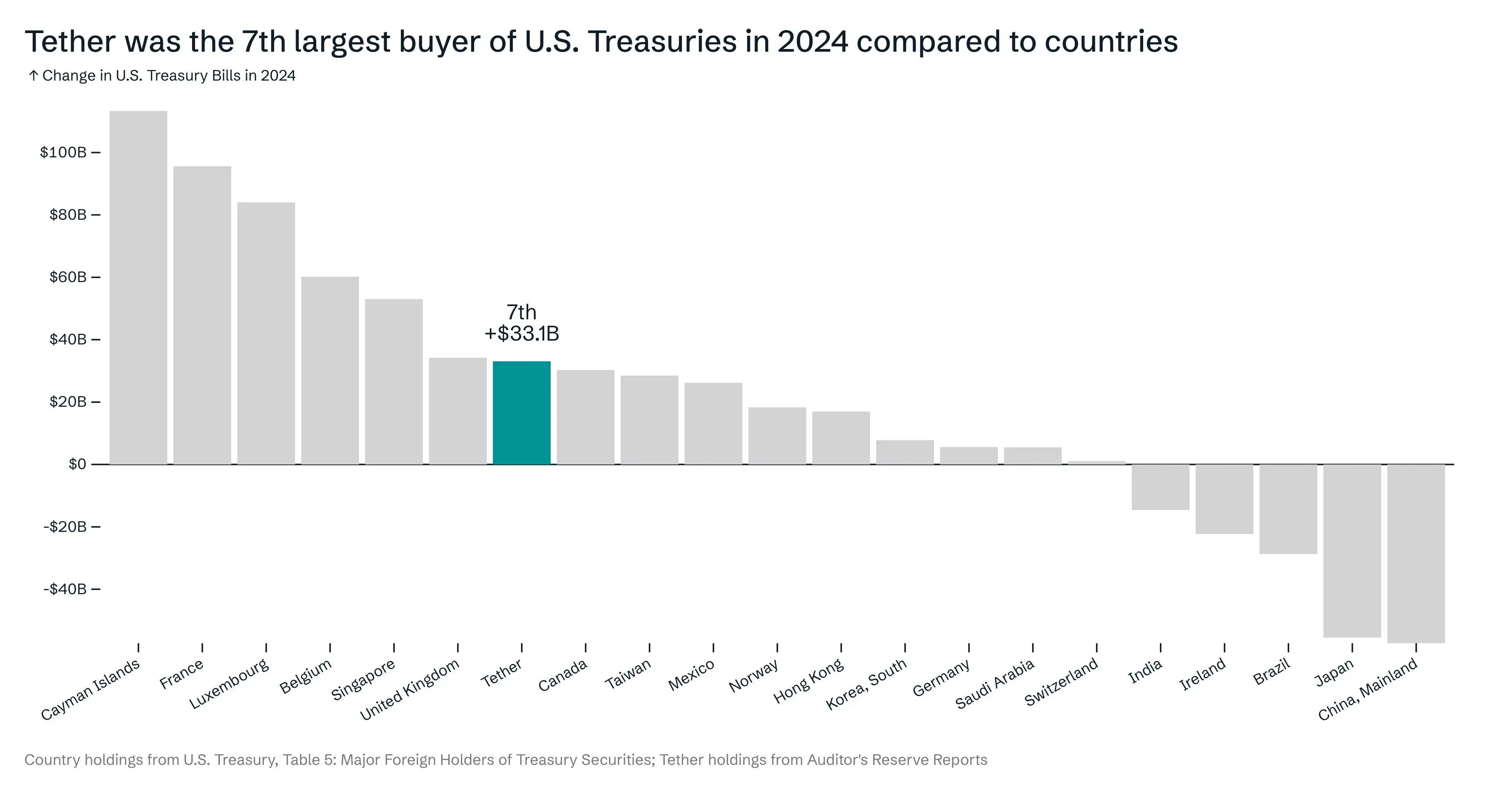

Furthermore, the continued growth of stablecoins may become an important source of demand for short-term U.S. Treasuries in the context of China and other countries potentially using U.S. Treasuries as a tool for geopolitical games. Although it is difficult to quantify the direct impact of stablecoins on the yield curve, Tether and Circle already hold more than $120 billion in short-term U.S. Treasuries (about 3 months), proving that their purchasing power on the short end of the yield curve is stable and sustainable.

Future Outlook: Plasma’s Role in Core Financial Infrastructure

Plasma's vision is to become the core financial infrastructure of the digital age, just as TCP/IP became the core infrastructure of the information age. This vision is ambitious but reasonable. Its goal is not to create a new currency, but to upgrade the way USD₮, the current dominant digital dollar, circulates around the world and further consolidate the dollar's dominance.

However, the journey has just begun. Plasma needs to prove its security and reliability in large-scale use scenarios and attract a wide range of validators, not limited to current crypto users, but also new user groups - whether individual users, fintech companies or large institutions. At the same time, Plasma will also face competition from existing mainstream platforms such as Tron, Solana and various Ethereum second-layer networks, as well as new chains built specifically for payment scenarios. But given the global scale of the payment market, this field is large enough to accommodate multiple winners. In an industry where everyone is always chasing the next general L1 or the next wave of memecoin craze, Plasma's strategy of focusing on stablecoins seems pragmatic and clear.

In summary, Plasma is not trying to "reinvent the wheel". What it does is leverage USD₮ - the world's largest and most liquid USD stablecoin - and promote its global spread and adoption through a zero-fee transfer mechanism. It is not controversial that stablecoins have proven to be one of the core killer applications in the crypto industry. We believe that the aggregation and spread of USD₮ on Plasma will not only improve the efficiency of USD₮ distribution, but also bring important secondary and tertiary effects, thereby injecting vitality into further innovation and economic activity on the chain. For all the above reasons, we believe that Plasma is expected to occupy an important position in this trillion-dollar opportunity.

Click here to learn about BlockBeats' BlockBeats job openings

Welcome to join the BlockBeats official community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia