1. Global macroeconomic variables reshape asset pricing paths: inflation, the US dollar, and a new round of capital competition

In the second half of 2025, global financial markets entered a new era dominated by macroeconomic variables. Over the past decade, loose liquidity, global collaboration, and technological dividends formed the three pillars of traditional asset pricing. However, in this cycle, these conditions are undergoing a systematic reversal, and the pricing logic of the capital market is undergoing a profound reshaping. As a leading indicator of global liquidity and risk appetite, crypto assets are seeing their price trends, fund structure, and asset weights driven by new variables. The three most critical variables are the stickiness of structural inflation, the structural weakening of the US dollar's creditworthiness, and the institutional differentiation of global capital flows.

First, inflation is no longer a short-term volatility that can be quickly suppressed; it is beginning to exhibit stronger "stickiness." In developed economies, particularly the United States, core inflation has consistently remained above 3%, well above the Federal Reserve's 2% target. The core reason for this phenomenon lies not in simple monetary expansion but rather in the entrenching and self-amplifying effects of structural cost drivers. While energy prices have returned to a relatively stable range, the surge in capital expenditures driven by artificial intelligence and automation, the rising prices of upstream rare metals in the transition to green energy, and rising labor costs due to the reshoring of manufacturing have all become endogenous sources of inflation. At the end of July, the Trump administration reaffirmed the full reimposition of high tariffs on bulk industrial and technology products from China, Mexico, Vietnam, and other countries, effective August 1st. This decision not only signals the continuation of geopolitical tensions but also suggests that the US government considers inflation an acceptable "strategic cost." Against this backdrop, the costs of raw materials and intermediate goods faced by US companies will continue to rise, driving a second wave of price increases in consumer goods, creating a pattern of "policy-driven cost inflation." This is not overheated inflation in the traditional sense, but policy-driven embedded inflation, the persistence of which and its penetration into asset pricing will be far stronger than in 2022.

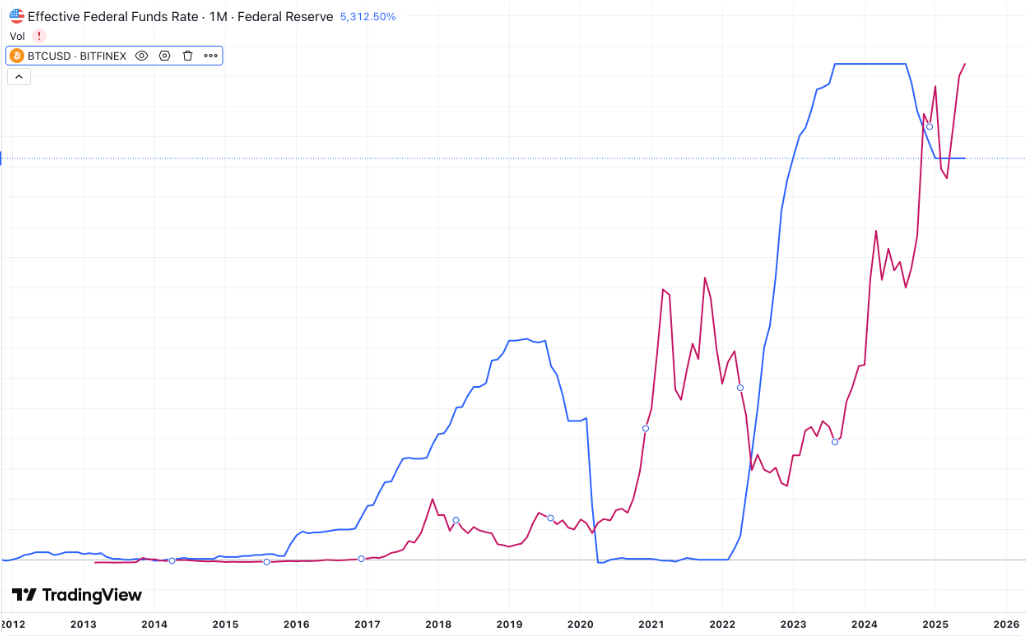

Secondly, with inflation still high, the Federal Reserve is unlikely to loosen its interest rate policy quickly. Market expectations indicate that the federal funds rate will remain elevated above 5% until at least mid-2026. This has led to repressive pricing in traditional stock and bond markets: the bond yield structure has inverted, duration products have suffered severe losses, and the stock market faces a continued increase in the discount factor in valuation models. In contrast, crypto assets, particularly Bitcoin and Ethereum, are valued more based on a complex model of "expected growth, scarcity, and consensus anchor." These assets are not directly constrained by traditional interest rate instruments. Instead, their scarcity and decentralization have attracted more investment in high-interest-rate environments, demonstrating counter-cyclical pricing behavior. This characteristic has gradually transformed Bitcoin from a "highly volatile speculative asset" to an "emerging alternative store of value asset."

More profoundly, the US dollar's global anchoring role is facing structural weakening. The US fiscal deficit continues to widen, exceeding $2.1 trillion in the second quarter of 2025, an 18% year-on-year increase and a record high for the same period. At the same time, the US's role as a global settlement hub is facing challenges from decentralization. Countries such as Saudi Arabia, the UAE, and India are promoting large-scale currency pegs, with cross-border payment systems such as the RMB-dirham and rupee-dinar systems beginning to replace some US dollar settlements. This trend reflects not only the cyclical damage inflicted by US dollar policies on non-US economies but also these countries' active attempts to decouple from the "single currency anchor." In this environment, digital assets have become neutral, programmable, and decentralized alternative media of value. For example, stablecoins such as USDC and DAI are rapidly expanding in over-the-counter (OTC) transactions and cross-border B2B payments in Asian and African markets, becoming a digital extension of the "underground dollar system" in emerging markets. Bitcoin, on the other hand, has become a vehicle for capital flight and a safe haven for global funds against currency devaluation. For example, in Argentina, Nigeria, and Turkey, residents' purchasing power premium for BTC has reached over 15%, reflecting genuine capital demand for risk aversion.

It's worth noting that while the trend toward de-dollarization continues to accelerate, the dollar's internal credit system is also showing signs of fatigue. In June 2025, Moody's and Fitch simultaneously downgraded the outlook for the US's long-term sovereign credit rating to "negative," citing "structurally irreversible long-term fiscal deficits" and "political polarization impacting budgetary implementation" as the primary reasons. The rating agencies' systemic warnings about US Treasury bonds triggered increased volatility in the US Treasury market, leading to a shift in safe-haven funds seeking to diversify their reserve holdings. Purchases of gold and Bitcoin ETFs surged during the same period, demonstrating a preference by institutional investors for reallocation to non-sovereign assets. This behavior reflects not only a demand for liquidity but also a "valuation flight" from the traditional asset class. With US stocks and bonds increasingly overvalued, global capital is seeking alternative anchors to rebalance the "systemic safety" of its portfolios.

Finally, institutional differences in global capital flows are reshaping the boundaries of asset markets. Within the traditional financial system, tightening regulation, valuation bottlenecks, and rising compliance costs are limiting the expansion of institutional capital. In the crypto sector, particularly driven by the approval of ETFs and the relaxation of audit regulations, crypto assets are gradually entering a phase of "compliance legitimacy." In the first half of 2025, several asset management companies received approval from the US SEC to launch thematic ETFs targeting crypto assets such as SOL, ETH, and AI. Funds are indirectly entering the blockchain through financial channels, reshaping the distribution of funds across assets. This phenomenon reflects the increasing dominance of institutional frameworks over the flow of capital.

Therefore, we can see an increasingly clear trend: changes in traditional macroeconomic variables—including the institutionalization of inflation, the blunting of the US dollar's creditworthiness, the prolonged high interest rates, and the policy-driven diversion of global capital—are collectively driving the dawn of a new era of pricing. In this era, value anchors, credit boundaries, and risk assessment mechanisms are all being redefined. Crypto assets, particularly Bitcoin and Ethereum, are gradually moving from a liquidity bubble to a stage of institutional value inheritance, becoming direct beneficiaries of the marginal restructuring of the macro-monetary system. This also provides a foundation for understanding the underlying logic of asset price movements in the coming years. For investors, updating their cognitive structure is far more critical than short-term market analysis. Future asset allocation will no longer simply reflect risk appetite but rather a deeper understanding of institutional signals, monetary structure, and the global value system.

2. From MicroStrategy to Listed Company Financial Reports: The Institutional Logic and Diffusion Trends of Coin-to-Stock Strategies

The most significant structural shift in the crypto market during the 2025 cycle stems from the rise of the "coin-to-equity strategy." From MicroStrategy's early attempts to use Bitcoin as a corporate reserve asset to the increasing number of publicly listed companies proactively disclosing details of their crypto asset allocations, this model has evolved from an isolated financial decision to a strategic, institutionally embedded corporate behavior. Coin-to-equity strategies not only open up channels for liquidity between capital markets and on-chain assets but also spawn new paradigms in corporate financial reporting, equity pricing, financing structures, and even valuation logic. Their widespread adoption and capitalization effects have profoundly reshaped the funding structure and pricing models of crypto assets.

Historically, MicroStrategy's Bitcoin strategy was viewed as a "go-for-broke" high-volatility gamble, particularly during the sharp decline in crypto assets between 2022 and 2023, which led to widespread skepticism about the company's stock price. However, in 2024, as Bitcoin prices reached record highs, MicroStrategy successfully restructured its financing strategy and valuation model through a structured "coin-stock linkage" strategy. This strategy hinges on the synergistic drive of three flywheel mechanisms: the first is "coin-stock resonance," whereby the company's Bitcoin holdings, through rising prices, continuously amplify the net asset value of its crypto assets in its financial statements, thereby boosting its stock price and, in turn, significantly reducing the cost of subsequent financing (including additional issuances and bonds); the second is "equity-debt synergy," which introduces diversified funding through the issuance of convertible bonds and preferred stock, while leveraging the market premium of Bitcoin to reduce overall financing costs; and the third is "coin-debt arbitrage," which combines traditional fiat debt structures with the appreciation of crypto assets to facilitate cross-cycle capital transfers over time. After this mechanism was successfully verified in MicroStrategy, it was quickly imitated and structurally transformed by the capital market.

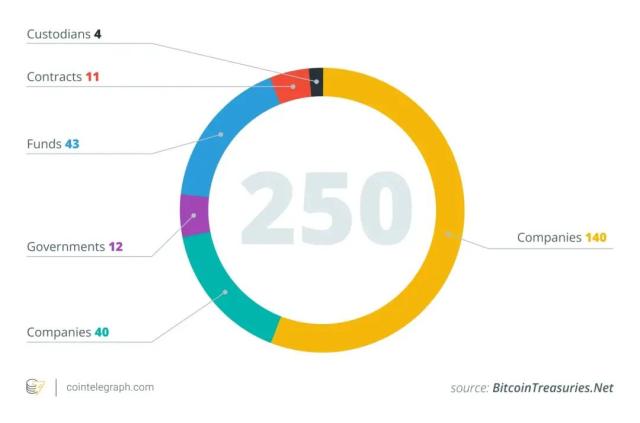

By 2025, the cryptocurrency-to-equity strategy is no longer limited to experimental allocations within a single company. Instead, it has spread to a wider range of listed companies as a financial structure with both strategic and accounting advantages. According to incomplete statistics, as of the end of July, over 35 listed companies worldwide had explicitly included Bitcoin on their balance sheets, 13 of which also included ETH, and another five were experimenting with mainstream Altcoin such as SOL, AVAX, and FET. The common characteristics of this structural allocation are: on the one hand, it creates a closed-loop financing loop through capital market mechanisms; on the other hand, it uses crypto assets to enhance corporate book value and shareholder expectations, thereby boosting valuations and equity expansion capabilities, creating a positive feedback loop.

This proliferation is primarily driven by changes in the institutional environment. The GENIUS Act and the CLARITY Act, officially enacted in July 2025, provide a clear and compliant path for listed companies to allocate crypto assets. The CLARITY Act's "mature blockchain system" certification mechanism directly categorizes core crypto assets like Bitcoin and Ethereum as commodities, divesting the SEC of their securities oversight and creating legal legitimacy for including these assets in corporate financial reports. This means that listed companies no longer need to list their crypto assets as "financial derivatives" in their risk accounts. Instead, they can account for them as "digital commodities" within long-term assets or cash equivalents, and even, in certain scenarios, include them in depreciation or impairment charges, thereby reducing accounting volatility risk. This shift allows crypto assets to join traditional reserve assets like gold and foreign currency reserves and enter mainstream financial reporting.

Secondly, from a capital structure perspective, the crypto-equity strategy creates unprecedented financing flexibility. Under the Federal Reserve's high interest rate environment, financing costs for traditional businesses remain high, making it particularly difficult for small and medium-sized growth companies to leverage expansion through low-cost debt. Companies allocating to crypto assets, however, can leverage the valuation premiums generated by rising stock prices to not only achieve higher price-to-sales and price-to-book ratios (PS and PB) in the capital markets, but can also use crypto assets as collateral to participate in new financial operations such as on-chain lending, derivatives hedging, and cross-chain asset securitization. This creates a dual-track financing system: on-chain assets provide flexibility and yield, while off-chain capital markets provide scale and stability. This system is particularly suitable for Web3-native businesses and fintech companies, allowing them to achieve significantly greater capital structure flexibility within a compliant framework than traditional approaches.

Furthermore, crypto-stock strategies have triggered a shift in investor behavior. With crypto assets widely allocated to public company balance sheets, the market has begun to re-price these companies' valuation models. Traditionally, corporate valuations are based on metrics such as profitability, cash flow expectations, and market share. However, when companies report significant crypto holdings, their stock prices begin to exhibit a strong correlation with the price of the cryptocurrency. For example, the share prices of companies like MicroStrategy, Coinbase, and Hut8 have far exceeded industry averages during Bitcoin's upward cycle, demonstrating a strong premium for the "gold content" of crypto assets. Simultaneously, a growing number of hedge funds and structured products are viewing these "high-coin-weighted" stocks as ETF alternatives or proxies for crypto exposure, increasing their allocations within traditional portfolios. This behavior has structurally driven the financialization of crypto assets, enabling Bitcoin and Ethereum to exist not only as assets in their own right but also as indirect circulation channels and derivative pricing functions in the capital market.

Furthermore, from a regulatory strategic perspective, the proliferation of crypto-to-equity strategies is also seen as an extension of the US's efforts to maintain its dominance over the US dollar in the global financial order. Amidst the growing global trend of CBDC (central bank digital currency) pilots, the continued expansion of RMB cross-border settlement, and the European Central Bank's testing of a digital euro, the US government has not actively launched a federal CBDC, instead opting to shape a decentralized US dollar network through stablecoin policies and a "regulatable crypto market." This strategy requires a compliant, high-frequency market entry capable of large-scale deposits, and listed companies, as the bridge between on-chain assets and traditional finance, perfectly fulfill this role. Crypto-to-equity strategies can therefore be understood as the institutional underpinning of the US financial strategy of replacing the US dollar with non-sovereign digital currencies. From this perspective, listed companies' allocation of crypto assets is not simply an accounting decision, but rather a means of participating in the restructuring of the national financial architecture.

A more far-reaching impact lies in the global diffusion of capital structures. As more US-listed companies adopt crypto-to-equity strategies, listed companies in Asia Pacific, Europe, and emerging markets are following suit, seeking to secure compliance space through regional regulatory frameworks. Countries like Singapore, the UAE, and Switzerland are actively revising their securities laws, accounting standards, and tax regimes to open institutional channels for their companies to allocate crypto assets, creating a competitive landscape for crypto acceptance in global capital markets. It is foreseeable that the institutionalization, standardization, and globalization of crypto-to-equity strategies will be a key evolutionary direction for corporate financial strategies over the next three years and a key bridge for the deep integration of crypto assets with traditional finance.

In summary, from MicroStrategy's single breakthrough, to the strategic diffusion of multiple listed companies, and then to the standardized evolution at the institutional level, the coin-to-equity strategy has become a key channel connecting on-chain value and traditional capital markets. It represents not only an update in asset allocation logic and a restructuring of corporate financing structures, but also the result of a two-way game between institutions and capital. In this process, crypto assets have gained wider market acceptance and institutional security, completing the structural transition from speculative products to strategic assets. For the entire crypto industry, the rise of the coin-to-equity strategy marks the beginning of a new cycle: crypto assets are no longer just on-chain experiments, but have truly entered the core of global balance sheets.

3. Compliance Trends and Financial Structure Transformation: The Institutionalization of Crypto Assets Accelerates

In 2025, the global cryptoasset market is at a historic juncture where institutionalization is accelerating. Over the past decade, the crypto industry's trajectory has gradually shifted from "innovation outpacing regulation" to "compliance frameworks driving industry growth." Entering the current cycle, the core role of regulators has evolved from "enforcer" to "institutional designer" and "market guide." This reflects a renewed understanding of the structural influence of cryptoassets within national governance. With the approval of Bitcoin ETFs, the implementation of stablecoin legislation, the launch of accounting standards reform, and the capital market's reshaping of digital asset risk and value assessment mechanisms, compliance is no longer an external pressure on industry development, but rather an internal driving force behind the transformation of the financial structure. Cryptoassets are gradually being embedded in the institutional network of the mainstream financial system, completing the transition from "gray financial innovation" to "compliant financial components."

The core of this institutionalization trend is first and foremost the clarification and gradual relaxation of the regulatory framework. Between late 2024 and mid-2025, the United States passed the CLARITY Act, the GENIUS Act, and the FIT for the 21st Century Act, providing unprecedented clarity across a range of regulations, from commodity identification, token issuance exemptions, stablecoin custody requirements, KYC/AML regulations, to the applicable boundaries of accounting standards. The most structural impact of these changes is the "commodity" classification system, which designates foundational public blockchain assets like Bitcoin and Ethereum as tradable commodities, explicitly exempting them from securities law regulation. This classification not only provides a legal foundation for ETFs and the spot market but also creates a definitive compliance path for enterprises, funds, banks, and other institutions to incorporate crypto assets. This establishment of a "legal label" is the first step toward institutionalization and lays the foundation for subsequent tax treatment, custody standards, and financial product structure design.

At the same time, major global financial centers are competing to promote localized institutional reforms, transforming a competitive landscape from "regulatory troughs" to "regulatory highlands." Singapore's MAS and the Hong Kong Monetary Authority have both introduced multi-tiered licensing systems, incorporating exchanges, custodians, brokers, market makers, and asset managers into differentiated regulatory frameworks, establishing clear entry barriers for institutions. Abu Dhabi, Switzerland, and the United Kingdom are piloting on-chain securities, digital bonds, and composable financial products in their capital markets, enabling crypto assets to not only exist as an asset class but also gradually evolve into underlying elements of financial infrastructure. This "policy experimentation field" mechanism not only fosters innovation but also promotes the digital transformation of the global financial governance system, providing a new path for institutional upgrades and coordinated development for the traditional financial industry.

Driven by these institutions, the underlying logic of the financial structure has also undergone profound changes. First, there's the restructuring of asset classes. Crypto assets have steadily increased their share of global institutional allocations, rising from less than 0.3% in 2022 to over 1.2% in 2025, and projected to exceed 3% in 2026. While this proportion may seem modest, the marginal flows represented by these assets, representing tens of trillions of dollars in assets, are sufficient to reshape the liquidity and stability structure of the entire crypto market. Institutions like Blackstone, Fidelity, and BlackRock have not only launched BTC and ETH-related ETFs but have also incorporated crypto assets into their core asset allocation baskets through proprietary funds, fund-of-funds (FOFs), and structured notes. Crypto assets are gradually taking shape as risk hedging tools and growth engines.

Secondly, there's the standardization and diversification of financial products. Previously, cryptoasset trading was primarily limited to spot and perpetual contracts. However, driven by regulatory compliance, the market has rapidly evolved into a diverse range of products embedded within traditional financial structures. Examples include crypto ETFs with volatility protection, bond-like products pegged to stablecoin interest rates, on-chain data-driven ESG asset indices, and on-chain securitized funds with real-time settlement. These innovations not only enhance cryptoasset risk management capabilities but also lower the barrier to institutional participation through standardized packaging, allowing traditional funds to effectively participate in the on-chain market through compliant channels.

The third layer of financial structural transformation is reflected in clearing and custody models. Starting in 2025, the US SEC and CFTC jointly recognized three "compliant on-chain custodians," formalizing the bridge between on-chain asset ownership, custodial responsibilities, and legal accounting entities. Compared to previous custody models based on centralized exchange wallets or cold wallets, compliant on-chain custodians utilize on-chain verifiable technology to achieve tiered asset ownership, isolated trading permissions, and embedded on-chain risk control rules, providing institutional investors with risk control capabilities approaching those of traditional trust banks. This shift in the underlying custody structure is a key component of institutionalized infrastructure development, determining whether the entire on-chain financial system can truly support complex structured operations such as cross-border settlement, mortgage lending, and contract settlement.

More importantly, the institutionalization of crypto-assets is not only a process of regulatory adaptation to the market but also an attempt by sovereign credit systems to incorporate digital assets into macro-financial governance structures. With stablecoin daily trading volume exceeding $3 trillion and beginning to assume de facto payment and clearing functions in some emerging markets, central banks' attitudes toward crypto-assets have become increasingly complex. On the one hand, central banks are promoting the development of CBDCs to strengthen their monetary sovereignty; on the other hand, they are adopting an open management approach of "neutral custody + strong KYC" for some compliant stablecoins (such as USDC and PYUSD), effectively allowing them to assume international settlement and payment clearing functions within certain regulatory boundaries. This shift in attitude means that stablecoins are no longer a target of central bank opposition, but rather one of the institutional containers in the reconstruction of the international monetary system.

This structural shift is ultimately reflected in the "institutional boundaries" of crypto assets. The market in 2025 will no longer be divided by the discrete logic of "crypto- blockchain circle - outside the circle," but will instead be forming three continuous tiers: "on-chain assets - compliant assets - financial assets." Channels and mapping mechanisms exist between each tier, meaning that each asset class can enter the mainstream financial market through some institutional pathway. Bitcoin has evolved from a native on-chain asset to the underlying underlying asset of ETFs, while Ethereum has evolved from a smart contract platform asset to a general-purpose computational financial protocol token. Even the governance tokens of some DeFi protocols have been structured and packaged as hedge fund risk exposure tools to enter FOF fund pools. This flexible evolution of institutional boundaries has made the definition of "financial assets" truly cross-chain, cross-national, and cross-institutional systems possible for the first time.

From a broader perspective, the institutionalization of crypto assets is essentially the adaptation and evolution of the global financial structure in the face of digitalization. Unlike the Bretton Woods and petrodollar systems of the 20th century, the 21st-century financial structure is reshaping the fundamental logic of resource flows and capital pricing through a more distributed, modular, and transparent approach. Crypto assets, as a key variable in this structural evolution, are no longer merely an outlier but rather digital resources that are manageable, auditable, and taxable. This institutionalization process is not a sudden policy shift, but rather a systematic evolution involving the coordinated interaction of regulators, markets, businesses, and technology.

Therefore, it is foreseeable that the institutionalization of crypto assets will deepen, and over the next three years, three coexisting models will emerge across major economies worldwide: One is the "market openness + prudent regulation" model, led by the United States, centered around ETFs, stablecoins, and DAO governance; another is the "restricted access + policy guidance" model, exemplified by countries like China, Japan, and South Korea, which emphasizes central bank control and licensing; and finally, the "financial intermediary pilot zone" model, exemplified by countries like Singapore, the United Arab Emirates, and Switzerland, which provides institutional intermediaries between global capital and on-chain assets. The future of crypto assets will no longer be a struggle between technology and institutions, but rather a restructuring and absorption of technology by institutions.

4. Conclusion: From Bitcoin's decade to the coin-stock linkage, welcoming the new landscape of encryption

In July 2025, Ethereum celebrated its tenth anniversary, and the crypto market moved from early experimentation to institutionalization. The widespread launch of coin-stock strategies symbolized the deep integration of traditional finance and crypto assets.

This cycle is no longer just a market launch, but also a reconstruction of structure and logic: from macro-currency to corporate assets, from crypto infrastructure to financial governance models, crypto assets have truly entered the scope of institutional asset allocation for the first time.

We believe that over the next two to three years, the crypto market will evolve into a ternary structure characterized by "on-chain native returns, compliant financial interfaces, and stablecoin-driven growth." The coin-to-equity strategy is just the beginning; deeper capital integration and governance model evolution are just beginning.