Author: David, TechFlow

Hong Kong is accelerating the legislative process for stablecoins.

On July 29, the Hong Kong Monetary Authority released the Consultation Conclusions and Guidelines for Licensed Stablecoin Issuers, the Consultation Conclusions and Guidelines on Anti-Money Laundering and Counter-Terrorist Financing (Applicable to Licensed Stablecoin Issuers), and two institutional explanatory documents, providing detailed implementation rules for the stablecoin regulatory system that will take effect on August 1.

Previously, the Hong Kong Legislative Council formally passed the Stablecoin Ordinance on May 21, establishing a licensing system for stablecoin issuers.

From the passage of the ordinance to the release of supporting guidelines and formal implementation, Hong Kong completed the "last mile" of its stablecoin regulatory system in less than three months.

What exactly is the relationship between these documents?

From the above, we can see that this comprehensive regulatory system consists of one ordinance (Stablecoin Ordinance), two sets of guidelines (and their consultation conclusions), and two explanatory documents, forming a complete chain from legal foundation to implementation details to operational guidelines.

Specifically, the entire document system includes:

1 Basic Law: Stablecoin Ordinance (released in May)

2 Regulatory Guidelines: Guidelines for Licensed Stablecoin Issuers, Guidelines on Anti-Money Laundering and Counter-Terrorist Financing

2 Consultation Conclusions: Recording the public consultation process and HKMA's responses for the above two sets of guidelines

2 Explanatory Documents: Summary of Stablecoin Issuer Licensing System, Summary of Transitional Provisions for Existing Stablecoin Issuers

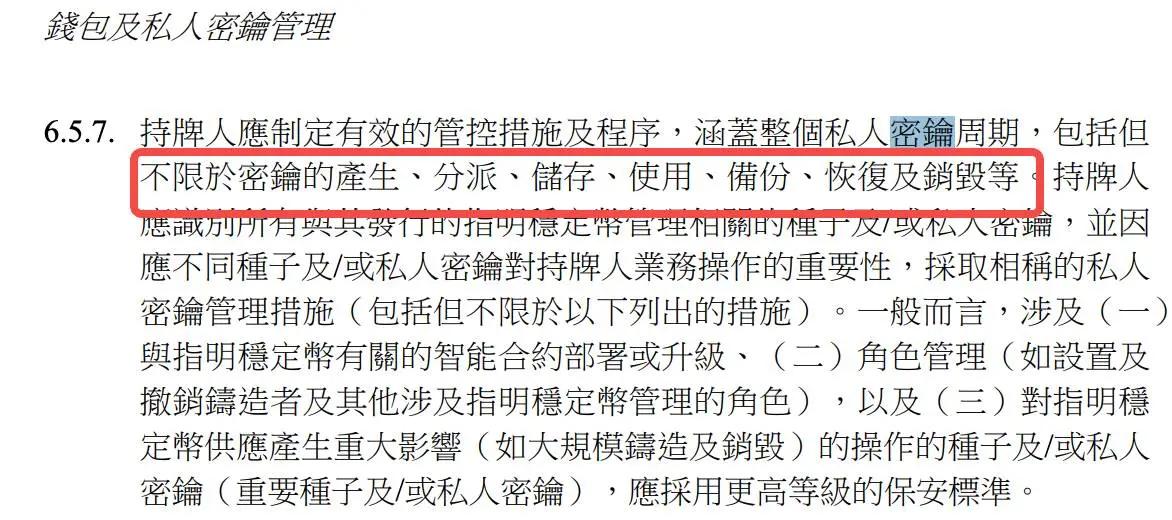

From key generation to destruction, from physical security to leak response, 12 specific requirements almost cover every stage of the private key lifecycle.

For instance, "Critical private keys must be used in an isolated environment" - this means private keys used for minting and destroying stablecoins cannot access the internet and must be operated in a completely offline environment;

"Key usage requires multi-party authorization" - no single individual can independently use critical private keys;

"Key storage media must be placed in Hong Kong or in a location approved by the monetary authority" - this directly excludes the possibility of hosting private keys overseas.

These requirements show that the monetary authority is not simply applying traditional financial regulation, but truly understanding the characteristics and risks of blockchain technology. To some extent, this guide can be viewed as a regulatory version of "enterprise-level private key management best practices".

The requirements for smart contract auditing are equally strict. Issuers must hire a "qualified third-party entity" to audit smart contracts during deployment, redeployment, or upgrade, ensuring the contract "executes correctly", "matches expected functionality", and is "highly confident of no vulnerabilities or security defects". Considering that the smart contract audit industry is still in its early stages of development, the definition of "qualified" may become a challenge in practice.

In customer identity authentication, the regulatory requirements reflect a fusion of Web3 and traditional KYC.

On one hand, issuers must complete "relevant customer due diligence" before providing services; on the other hand, they must "only transfer stablecoins to customer pre-registered wallet addresses". This design attempts to find a balance between anonymity and compliance.

Operational Standards: The "Bankification" Path of Stablecoins

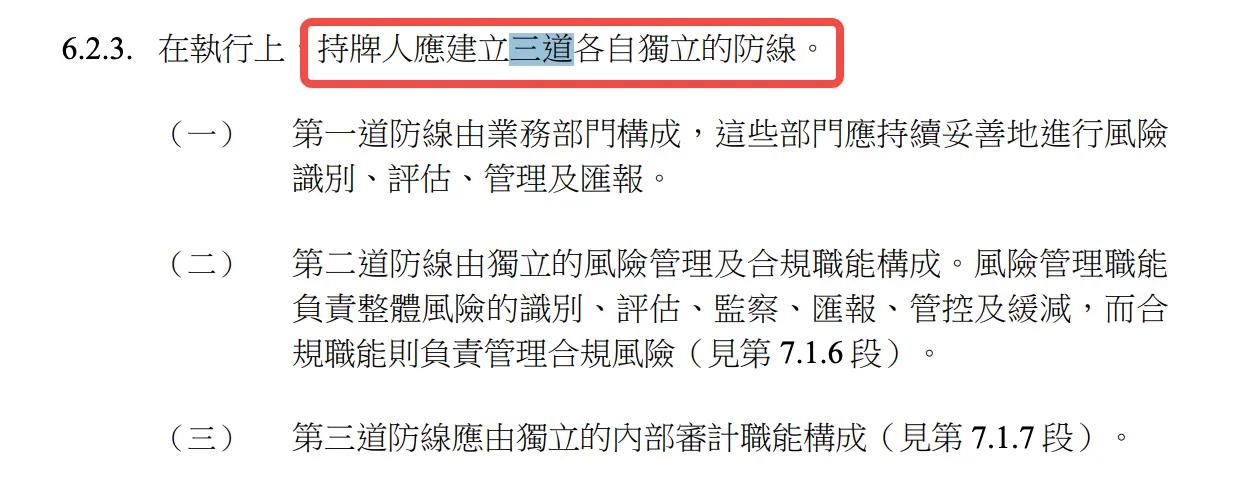

"T+1 redemption", "pre-registered accounts", "three lines of defense" - from these requirements in the original document, it can be seen that Hong Kong wants stablecoin issuers to align with traditional financial institutions' operational standards and maximize risk control.

First, let's look at the redemption timeline.

"Effective redemption requests should be processed within one business day after receipt" - this T+1 requirement is stricter than many existing stablecoins. Tether's terms of service reserve the right to delay or refuse redemption, while Hong Kong's regulations elevate timely redemption to a legal obligation.

However, this "bankification" is not a simple replication. The regulatory guide also reserves flexibility for "exceptional circumstances" - if redemption needs to be delayed, written consent from the monetary authority must be obtained in advance. This mechanism is similar to the banking industry's "suspension of withdrawal" clause, providing a buffer for system stability under extreme market conditions.

The three-line defense risk management system directly borrows mature practices from the banking industry:

The first line of defense is the business department, the second line is independent risk management and compliance functions, and the third line is internal audit. For many Web3 native teams, this means a fundamental change in organizational structure - you can no longer be a flat technical team but must establish a hierarchical organization with clear responsibilities.

Particularly noteworthy is the management of third-party risks.

Whether it's reserve asset custody, technical service outsourcing, or stablecoin distribution, all arrangements involving third parties must undergo strict due diligence and continuous monitoring. The regulatory guide even requires that if a third-party service provider is outside Hong Kong, the issuer must assess the local regulatory authority's data access rights and promptly notify the monetary authority when requested.

KYC Myth: Must Token Holders Be Identified?

Currently, on social media, everyone is most concerned about the KYC issue.

Previous analyses have pointed out that the regulatory document's strict requirement for any stablecoin holder to undergo identity verification also means being identified.

Let's look at the original text of the document:

Although the regulatory guide distinguishes between "customers" and "holders", careful analysis reveals this distinction is more like a "trap" - you can acquire and hold stablecoins relatively freely, but to realize its core value (redeeming fiat currency), KYC is almost unavoidable.

[Translation continues in the same manner for the rest of the text]The licensing threshold of 25 million is not low, but compared to Hong Kong's virtual asset trading platform's capital requirement of 500 million USD, it is relatively reasonable; the technical requirements are detailed, but also clearly accept innovative concepts like "tokenized assets"; the operational standards are strict, but also reserve emergency mechanisms for market fluctuations.

More importantly, this regulatory framework demonstrates Hong Kong's understanding of the nature of stablecoins:cois not cryptocurrency, a but a key infrastructure connecting traditional finance and the digital economy. Therefore, regulatory standards must be high enough to maintain financial stability, but also flexible enough to adapt to technological innovation.

For market participants, the signal convebythe guide is very clear:

Hong Kong welcomes responsible innovators, but be prepared to accept strict regulation.

Institutions hoping to issue stablecoins in Hong Kong need to carefully assess whether they have the necessary financial strength, technical capabilities, and compliance resources.

For the entire industry,, Hong Kong's practice provides an important reference: stablecoin regulation is not about ststifling innovation, but about providing sustainable soil for innovation.

When regulatory rules are clear and enforcement standards are explicit, compliance costs are predictable, and the boundaries of innovation are explorable.

This may be the key to Hong Kong maintaining its competitiveness as an international financial center in the digital asset era.

Recommended reading:

Pump.fun's Three-Part Decline: Legal Hunting, Token Price Halved, Trust Collapsed